Master your fundamental research. Join 79,627 investors who trust our platform and content.

Save 54+ hours of fundamental research with free access to Stock Card.

We only ask your name and email address.

Did you know New York Stock Exchange traders have a long-standing tradition of celebrating each year's last trading day with a song that goes back to the great depression in the 1930s? The song’s lyrics are pretty interesting. Their main message is to encourage traders to look into the future because things will surely improve in the new year. It goes like this: Wait till the sun shines, Nellie And the clouds go a-drifting by We will be happy, Nellie Don't you cry… It gets even more interesting when you hear the NYSE floor traders sing it (watch here). There is something positive and encouraging in hearing fellow investors’ message of a better future. Listening to the song has made me wonder how we all can turn 2024 into a better year for our portfolios as the NYSE traders' song promises. In other words what should our New Year investing resolution be. What Is Your Investing Resolution?I’ll let you in on my 2024 investing resolution: Getting 1% better at investing every day.

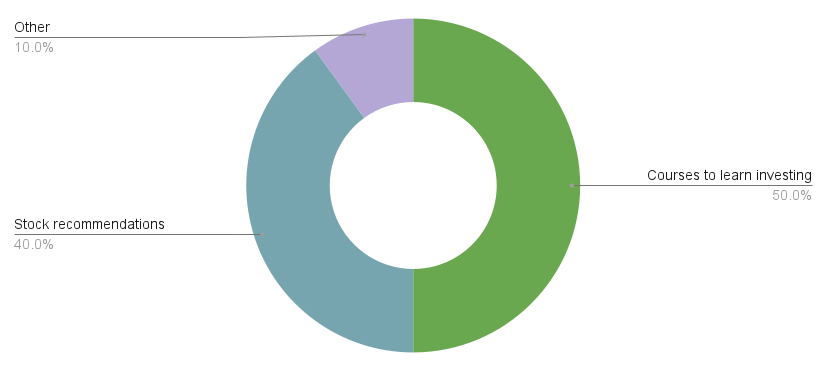

Why did I choose this as my resolution? Because working on ourselves and our skills is the only thing in investing that is under our control. We can’t predict the market. We can’t forecast the macroeconomic factors. We can’t even precisely calculate the fair share price of the individual stocks we own. That’s depressing, I know! But we have another choice! We can focus on the only thing in the stock market under our control: ourselves. Fascinatingly, getting 1% better in investing every day compounds our skills by 37 times in 365 days! The power of companding is amazing! By learning a new investing concept each day, researching a new stock every day, and learning about successful investors’ approaches to managing their money throughout the year, by the end of 2024, we will be 37 times better at investing. That’s my 2024 investing resolution. What’s yours? You can fill out this one-question form to officially commit to it. Remember than sharing resolutions increases the chances of reaching them. By the way, it takes a few seconds after you click for the resolution form to load on Stock Card’s website. When you share your investing resolution, we keep it on your account. We will check in with you regularly in 2024 to support you with resources and keep you accountable throughout the year so you can make your 2024 portfolio the best one yet. Happy New Year!  Last week, I shared a user town hall video to discuss some interesting data about our user base and ask everyone to respond to a 3-question survey. My goal was to learn about the content that is most useful to you and helps with your wealth-creation journey. The results are in, and it's pretty straightforward!  Half of you want courses to learn to invest, followed by 40% asking for stock recommendations. ✍️ Firstly, if you have yet to respond to the survey and DISAGREE with the above results, it's your chance to voice your opinion. The survey is still open, and you can chime in. CLICK HERE 📚 Secondly, at Stock Card, we aim to be YOUR best investing tool. We are in the process of developing several courses and will be publishing regular stock recommendations, write-ups, and live research sessions. Stay tuned for the announcements in the coming days. ❓ What about the 📺 YouTube channel and 🎙️ podcast show?They continue to air with some changes to the programming. Traditionally, money and topics related to money have been kept serious and dry. There is no reason for money stories to be boring. My goal is to make money content entertaining, educational, and more accessible to you and other retail investors out there. Stay tuned because I'm excited to share fascinating money-related stories starting next week. Let's wrap up with two things:

I can't wait to implement the changes you have asked for!

Talk to you soon, – Hoda, Founder and CEO, StockCard.io This week I've been researching PayPal's stock. The debate over PayPal's future is quite dividing:

But the "new IBM" debate isn't new to Wall Street. Back in 2019, when Apple's iPhone price dropped, and the stock price crashed over 30% in a quarter, the media couldn't help but comparing Apple of 2019, with the IBM of 2013. I published a podcast episode back in 2019 and dug into the similarities between Apple and IBM. I just listened to the episode again, and really enjoyed it. I believe you'll also enjoy listening to that episode in anticipation of Saturday's PayPal episode. See you Saturday! P.S. Here's the original post from 2019 👇  What do Apple and IBM have in common? Well, in the past few years, the media is beating a new drum roll. It's not so much about IBM. Instead, it is about how Apple - once an arch enemy of IBM - is now morphing into a modern-day IBM. Considering the recent disappointing iPhone sales and the lack of any significant innovation by Apple in the past years, is it fair to assume that Apple is the new IBM and is destined for the same fate? Get all those questions answered by listening to the latest episode of Renegade Investors podcast. You are going to hear what Tim Cook had to say, understand how Apple's CFO talks about the company, explore Warren Buffett's point of view on both companies and dig deep into the state of affairs at IBM of 2013 vs. Apple of 2019.

The world potentially has a huge economic crisis on the horizon.

Its cause is China's real estate sector. You must have heard that Evergrande, one of China's largest real estate companies, has filed for Chapter 15 bankruptcy in the U.S. while figuring out the renegotiation of its $340 billion debt, which started a while ago. This is a huge amount of debt, roughly equal to 2% of China's GDP. Evergrande is one of many Chinese real estate developers in trouble. Another large property developer, Country Garden, has just warned investors of bankruptcy, with 43% of its debt coming due in the next 12 months, and it needs more cash to repay them. Even with that scale, it's difficult to understand why China's real estate sector problems can become a potential global economic crisis with a spillover impact on our portfolios. But if you dig deep, you'll see an intertwined web of problems and interdependancies across China and worldwide. This can be a big risk to individual investors even without direct investment in Chinese companies. We should first understand and then protect ourselves against it. Let's talk about that!

I'm Hoda Mehr, founder, and CEO of Stock Card, and on this blog and its accompanying YouTube channel and Podcast show, I share detailed fundamental analyses and interesting investment stories.

This post is part of our educational series to help you hone your fundamental investing skills. Catch up with the other post on How to Invest Like Buffett? or how to Find the Highest-Returning Stocks? Remember, this content is for education and sharing ideas and not advice to buy or sell any securities. Sign up for a free account on Stock Card to get notified of these blog posts, YouTube videos, and Podcast shows every week. We only ask your name and email address when you sign up.

China has a big problem in its real estate sector. Real estate is one of its primary growth drivers. We all have seen images and videos of China's ambitious, large-scale real estate projects over the last few years. The country has been spending on real estate staggeringly, from big new cities to airports and residential buildings. The sector represents 30% of China's GDP and is the most significant contributor to the country's economy.

This all-important sector has been facing a few challenges in recent years. The world became aware of the problem in 2021 when real estate giant Evergrande announced defaulting on $1.2 billion of its overseas bonds and planted the seeds of fear and panic in China's consumers. Two years later, in August 2023, Evergrande filed for Chapter 15 bankruptcy, allowing them to continue to deal with their massive $340 billion in debt in China and elsewhere without worrying about roughly $40B US debt and debt holder lawsuits and actions. And the debt issue isn't limited to Evergrande. Property developer Kaisa missed a $400M bond payment. In January 2022, Shimao Group defaulted on a $101M project loan, and Yuzhou Group requested a deferral for repayment of offshore bonds worth $582M. Most recently, in August 2023, Country Garden, another prominent property developer in China, spiraled into a similar debt crisis. This company carries $35B in debt, of which $15B, or 43%, is due in the next 12 months. Aside from bad planning and aggressive borrowing by these developers, they cannot meet their debt obligations because Chinese consumers are buying and investing in properties much less than before and have started selling what they already own. Most economists attribute this behavior to the consumers' pessimistic views and fear. Why Chinese Consumers Aren't Buying New Houses

For years, as China grew, the middle class grew their wealth with the country, many in the form of investing in and purchasing real estate. Here this: Homeownership reached 90% in 2020 in China, and as much as 70% of Chinese household wealth is tied to property ownership and investments. The real estate market in China is much bigger than the middle-class buying houses to live in. It has been known as a speculative market to make fast money.

You might have heard people have prepaid for Evergrande properties, and now, they are unsure if they can ever get the properties they were promised. Apparently, the largest source of income for property developers in 2020 were deposits and presales. That year, property developers raised over $1T from these two sources alone. Now, much of that investment may go down to zero, and investors may end up with significant losses. If that's not scary to an investor, then what is? It's easy to see why fear is spiraling in the market. That fear could result in lower demand for new properties, presales, and investment, which means lower prices. And we all know this: when real estate value starts decreasing, consumers see their wealth eroding, and their confidence in the real estate sector goes down with it. As a result, fewer buyers are in the market, further dragging down the prices. Existing homeowners and property investors would also decide to sell their homes to lock in their capital gain. Selling pressure pulls prices down, creating more panic-selling in the market. According to the official data, new-home prices have slipped 2.4% from a high in August 2021, and existing homes have dropped 6%. Unofficial numbers paint a much grimmer picture. For example, local agents have reported the value of real estate properties near Alibaba's HQ has dropped 25% or more. And prime real estate in Shanghai experienced a 15% drop or more compared to their peak in 2021 (source). As the property value goes down, demand and investments drop, and real estate developers run out of ways to make money to pay their debt. How Can China's Real Estate Crisis Spills Over The Entire Economy

Of course, those debt problems and bankruptcies are real issues for those companies' investors. More importantly, they will inevitably spill over to the rest of the market. Real estate developers have billions of dollars in debt to the banking system. If they can't sell their properties or have to sell them at significantly lower prices than anticipated, and if they can't get more loans to refinance their existing debt, which is true because of a policy in China that has been put in effect to manage property developers' debt, then they will have limited liquidity to pay their debt. From there, the domino effect starts. Banks that lend money to them will have a liquidity shortage. Customers who have deposits in those banks would rush to withdraw their money, and then those banks run out of cash and cannot cover their liabilities. The domino effect continues. Only a few months ago, we saw a real example of what a bank rush can do to a bank when California-based Silicon Valley Bank ran out of cash.

We already see the evidence of fear in the market. Country Garden's bondholders have already started panicking that they may not get the expected yield, selling their bonds in fear. For example, a $1B note by Country Garden due in January now trades at 13 cents on the dollar. So far, everything we've discussed is easy to understand and quite universal. This could have happened and has already happened in many other markets. But then, the story continues…

China's Real Estate Is a Huge Problem for Local Governments

China's real estate problem is also a huge problem for local governments because of how these local governments make money. In China, lands in the cities belong to the government. Companies buy the right to build a property over the land from the government for 70 years. Land-use sales revenue and real estate taxes represented 38% of the local government's revenue in 2020. This revenue will decrease if the real estate sector slows down. Some provinces received less than 20% of their annual land-use rights revenue in 2020. The real estate sector's dismay has already created a major budget issue for local governments.

The government is responsible for investing in the local infrastructure and is a big spender and a source of employment for locals, too. Lower revenue means lower spending and lower employment across Chinese provinces. So, as we discussed, the problem isn't just that Evergrande and Country Garden are running out of cash. The problem can be as big as the middle class losing their wealth, the banking system losing liquidity, and local governments losing revenue. As you can imagine, this is a HUGE and potentially catastrophic problem for the Chinese economy. Why The World Is Worried About China's Real Estate Problems

The International Monetary Fund (IMF) forecasts less than 4% GDP growth for China in the coming years. This growth rate indicates a more than 50% drop in the country's economic growth compared to the past four decades. A 50% drop in a country representing 18% of the global GDP is a big deal. Even more importantly, according to BCA Research, China has been the source of more than 40 percent of global economic growth over the past decade, compared with 22% from the U.S. and 9% from the eurozone. And, of course, China is a major trade partner to the U.S. Japan, Germany, India, Australia, and many other countries.

Bringing it to our portfolios, about 7.6% of the S&P 500's total revenue comes from China, according to FactSet. The tech companies in the S&P500 make 16% of their revenue from China. Semiconductor companies get 27% of revenue from the country. For example, the country represents 20% to 25% of Nvidia's revenue. The world economy is a massive web of interdependencies and connections. If China is in trouble, so is the rest of the world. How Can We Protect Ourselves Against China's Real Estate Risk

First of all, before panicking and taking your money out of the market in fear of China's threat to the world economy, we must say that there is still hope, and the Chinese government may very well be able to control the situation before it becomes a crisis. These measures include cutting the interest rate, giving mortgage-related incentives, and working with property developers to manage and refinance their debt.

Where there is more risk for individual investors is to invest without considering the hidden risk that may arise from the situation in China. As they say, the blade you don't see usually cuts the deepest. For example, suppose you are pouring money into Nvidia because it is skyrocketing due to the AI demand. As discussed earlier, you must also consider that a possible economic crisis in China is a risk to your Nvidia investment. In my view, the proper response to the possible economic crisis stemming from China or any other reasons is always the same:

See you next time!

Michael Burry, the man who foresaw the 2008 housing market crash, has seemingly decided to short the entire stock market once again! Despite his fame, Burry isn't that good at predictions if you follow some of his forecasts in recent years. But he is a very observant investor and makes logical arguments about discrepancies he sees between fundamentals and prices. What signs and signals has he seen this time around that prompted him to take such a daring stance again? And are there reasons to believe him this time and take similar actions to short the market and save our portfolios?

Let's talk about that!

I'm Hoda Mehr, founder, and CEO of Stock Card, and on this blog and its accompanying YouTube channel and Podcast show, I share detailed fundamental analyses and interesting investment stories.

This post is part of a series I started a few weeks ago to fundamentally research companies to manage my real-money portfolio. I've already researched Canopy Growth (CGC), Fastly (FSLY), Snap (SNAP) , Shopify (SHOP), Airbnb (ABNB), Unity (U), JD.com (JD), NVIDIA (NVDA) and several others. I also started sharing interesting investing-related stories. The first one was on what happens when the U.S. hit its 2% inflation target. More interesting stories are in the works. Remember, this content is for education and sharing ideas and not advice to buy or sell any securities. Sign up for a free account on Stock Card to get notified of these blog posts, YouTube videos, and Podcast shows every week. We only ask your name and email address when you sign up.

Berry shorting the U.S. market is one of those fascinating stock market stories. Whenever he makes such moves, the entire market takes note. But betting against the market isn't anything new for the big short investor. He's a pessimistic investor by nature and has made several bearish predictions since his successful bet against mortgage-backed securities during the great financial crisis.

Michael Burry's Marker Forecast Track Record

In September 2019, Michael told Bloomberg that index fund inflows were distorting stock and bond prices, and when the inflow reversed, the result would be catastrophic. His argument is correct. Over $11 trillion is invested in index funds, up from only $2 trillion a decade ago. The problem with indexes is that the decision is automatic. No one picks stocks, and money, in most cases, automatically flows into large indexes giving the stocks listed in indexes enormous price boosts. However, the prediction hasn't come to reality since 2019. For example, S&P 500 index ETF (SPY) had gone to more than $400 per share, up from $219 per share when Berry predicted the catastrophic consequence of flowing money into indexes.

In December 2020, Burry took it to Twitter (now X.com) to say that Tesla's stock price is ridiculously overpriced. Split-adjusted and despite volatility between 2020 and today, Tesla's stock price is still hovering slightly higher than its December 2020 price. Burry predicted a stock market crash in February 2021, after which the market went on for a few months of extraordinary rally thanks to the government stimulus and quantitative easing. While he was eventually correct, and we saw the rally ended in 2022, many considered his market crash predictions unreliable. Michael Burry's attention turned toward Bitcoin in March 2021, predicting a crash that was quite the opposite of Bitcon's rally to above $60,000 per coin price tag immediately after his prediction. Bitcoin price eventually crashed in 2022, but not before many lost faith in Burry's predictions. A pattern is emerging if we pay closer attention to all these predictions. Burry predicts catastrophic crashes based on logical evidence. But the markets do not necessarily follow his logic immediately. There is a time gap between when he shares his predictions and when they come true. Even in the case of Burry's bet against mortgage-backed securities, he initially saw the risks in 2005, at least 2 years earlier than the actual price drop. The secret to Burry's success is that he is patient even if the market takes the opposite direction in the short to mid-terms. Back to his latest put options, Michael Burry had purchased put contracts with an unknown strike price and exercise date, seemingly betting that the SPY and QQQ (top 100 Nasdaq stocks) would go down in prices at some point in the future. Before his option contracts expire, he has the right to sell his put options at the strike price, presumably higher than the SPY and QQQ price. We don't know anything about these options' dates and exercise prices. He can be quite patient and hold his put contracts for a long time to profit from the eventual crash he predicts is coming. We can simply interpret this move as a way for Burry to protect his hedge fund against an eventual crash. But Burry isn't the only one predicting a crash. Other investors seem to agree with Burry and have shared similar bearish sentiments in different ways. Bill Ackman's Market Forecast

Fellow hedge fund manager Bill Ackman is one of those. A few weeks ago, Ackman took it to Twitter (X.com) to explain his firm's belief that the U.S. treasuries were overbought. The evidence that supports Bill's argument when he made the statement was the $14B money inflow into iShares 20+ Year Treasury Bond ETF (ticker TLT) in 2023 alone. How exactly does Bill's bearish sentiment echo Michael Burry's bearish positions?

Bill is predicting that unlike many investors expecting the Fed to start cutting down interest rates, which in turn will boost the stock market prices, the opposite may be true. Bill believes the government's massive deficit would force it to issue more debt, and for the market to buy such debt, the government has to offer higher yields, which in return may mean lower equity prices. In a way, Bill Ackman and Burry agree on the possibility of lower equity prices and are hedging their risks differently but against similar forces. Morgan Stanley's Market Forecast

A recent market commentary by Morgan Stanley’s Global Investment Committee agrees with these two assessments. In summary, the committee believes that equity investors are too optimistic about interest rate cuts in the coming months, and the bond market doesn't support such a direction. The committee believes that the effect of the COVID-era stimulus has been lingering. Only now and in the coming months will we see the impact on consumer spending and corporate profits.

Cathie Wood's Market Forecast

That's the point that other investors agree with. In her monthly In the Know Updates, Ark Invest's Chief Investment Officer, Cathie Wood, warned investors of a possible hard landing for the U.S. economy. Cathie explained that companies would face pressure on their profits and profit margins for a few reasons, including hoarding the labor force and broad agreements between employees and employers in manufacturing and airline industries to increase salaries in response to inflation and union negotiations. Cathie Wood also believes the prices will start declining, adding more pressure on the company's profit margins. Those will be the reasons to see lower economic growth in the coming months, leading to negative sentiment in the stock market.

The question we should try to answer now is whether there are economic indicators that support Michael Burry, Bill Ackman, Morgan Stanley, and Cathie Wood's stances. Recession Economic Indicators

Historically, there are a few recession indicators:

So of the four economic indicators, the yield curve is the only one predicting a recession, and we have seen at least three investors agreeing with the yield curve. It seems most economic indicators do not agree with Michael Burry, Bill Ackman, Morgan Stanley, and Cathie Wood. What do we do with this contradiction between major economic indicators and prominent investors' stance to protect their portfolios? How To Crash Proof Our Portfolios

First of all, this is a good sign. The market typically goes to the extreme when everyone agrees on the same conclusion. A healthy market results from differences in opinions and the pull and push between these bearish and bullish sentiments.

Secondly, I know these investors all seem smart. But no one can predict the market. As much as it's hard to accept it, even smart investors such as Michael Burry can be wrong or at least be early in their predictions. Bill Ackman is famous for the wrong call he made about Herbal Life, and Cathie Wood, like any other investor, has lost lots of money in the market after the COVID rally came to an end, even though she has a team of smart analysts and they follow a diligent research process. We can't just follow them blindly, they can make mistakes in their conclusions. Where does that leave us? It leaves us with the old good wisdom we are all aware of:

Those are simple actions but not easy. If the market continues to rally, you'll regret not going all in. If the market crashes, you will regret some of the investments you've made now. Whatever you do, there will be reasons to regret and feel distressed. So, accept that there is no perfect investment decision. There is always risk in investing! There is no perfect investor. Invest slowly, steadily, in things you have done your research or have confidence in over a long period of time. I see you next time!

|

Categories

All

Archives

March 2024

|

RSS Feed

RSS Feed