Master your fundamental research. Join 79,627 investors who trust our platform and content.

Save 54+ hours of fundamental research with free access to Stock Card.

We only ask your name and email address.

|

The year was 2018-19, and Cannabis stocks were hot! All the cool kids were trading them. One of the market leaders, Canopy Growth was trading at $50 per share, and another, Tilray, was priced at more than $140 per share. Fast forward to 2023, and cannabis stocks have lost almost all their value. Both those market leader stocks are now down 98% from their all-time highs of 2018-19. Cannabis stocks are either destined for bankruptcy, and 100% value loss or they are deeply-discounted opportunities we should pay attention to now. Let's talk about that! I'm Hoda Mehr, founder and CEO of Stock Card, and on this blog and the accompanying YouTube channel and Podcast show, I share detailed fundamental analyses and interesting investment stories. The rise and fall of cannabis stocks is a classic story of investors running wild after the next big thing, pushing the prices to levels completely disconnected from the economic reality behind the companies and stocks in that sector. Then suddenly and violently, everything comes down crashing. Almost all similar stock market stories start with a new shiny sector and end with investors losing almost all their capital. I own a few shares of Canopy Growth in my portfolio, shining red hot at the bottom of the biggest losers. I purchased those shares in 2018 with a few justifications:

As Uncle Buffett puts it, if the price of hamburgers goes down, you don't stop eating them. You may even eat more. By the way, talking about my personal portfolio it's called Roll with Our CEO. This portfolio is our family's real-money stock market investments, beating the S&P 500 going back to 2014, and it's available to our VIP users to see and follow. If you'd like to access it, go to StockCard.io, create an account for free, and then use promo code "welcome" to receive 20% off of the Full VIP plan to see my entire portfolio. Click Here to Upgrade Of course, my portfolio isn't investment advice, neither are any of 100s of other real-money and idea portfolios on our platform. Use them as a resource for new ideas or validate your own ideas while doing your research. Now, how can Canopy Growth recover, grow and even thrive in the next ten years:

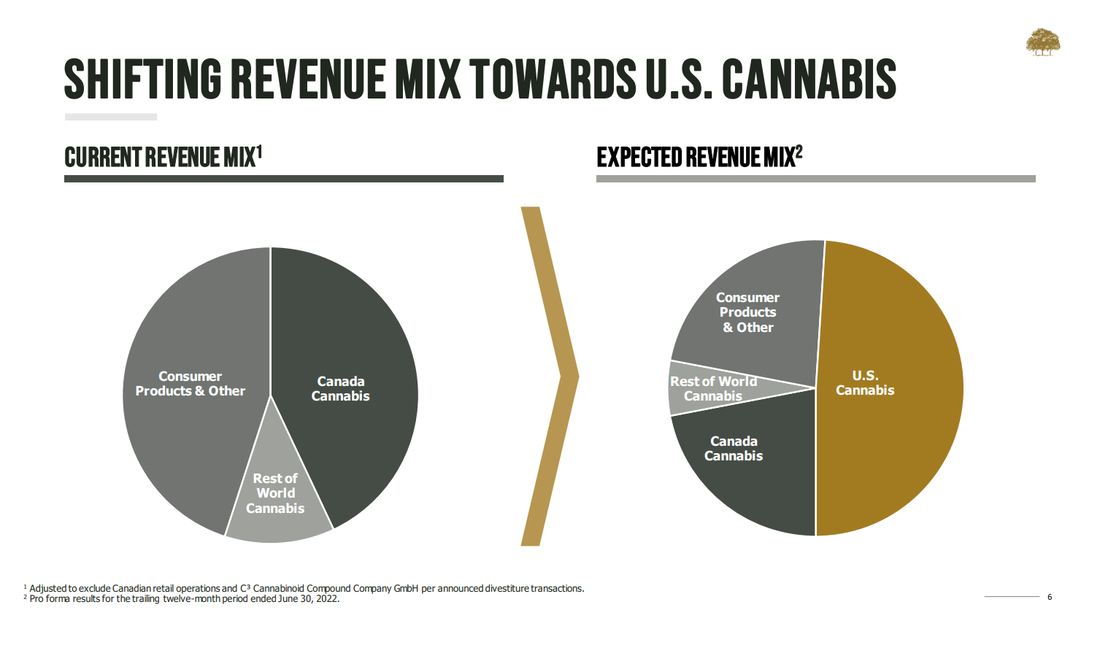

Cannabis Industry Market SizeDespite everything happening with Cannabis stocks, the global cannabis market is expected to grow by 24% between 2022 and 2026. The industry was hit by COVID-related restrictions, especially as farming and processing cannabis needs in-person human labor. But, with the pandemic restrictions almost entirely eliminated, the industry is back on a growth track. It's quite apparent that legalizing medical and recreational cannabis use is an important factor in driving growth. In the U.S. alone, 40 states and the District of Columbia have legalized medical use, and 21 states allow recreational use. Even in a state like Texas, bills are advancing to legalize medical use. While Federal level legalization is unlikely this year, President Biden has asked the Secretary of Health and the Attorney General to review cannabis's classification as a Schedule II drug which is good progress toward ultimate legalization. It also opens the door for more pharmaceuticals to start researching it as an ingredient which can lead to a significant demand increase by pharmaceuticals down the road. So, despite the stock price crashes, the cannabis industry is growing steadily. Canopy Growth (CGC) Fundamental AnalysisIf Canopy Growth can grow its revenue by at least 50% of the overall market rate, the stock will have major growth potential. Especially if you compare that with its 2022 5% revenue drop. The question is whether Canopy Growth and its management believe that can achieve such growth. Let's see what they had to say in their latest investor presentation. The company aspires to generate 50% of its revenue from the U.S. market instead of its current concentration in Canada. It's been investing in a portfolio of consumer-facing brands such as Acreage, Wana, Jetty, and TerrAscend, and plans to grow its own brands in the U.S. As a matter of fact, the company calls the U.S. legalization a once-in-a-generation opportunity.  That's a good strategy. However, the company outlined several restructuring requirements to simplify its organization, especially related to Constellation Brands' investment in the company and acquisition deals related to Acerage, Jetty, and Wanna. It's also moving away from retail operations by divesting from its Canadian retail business to cut costs and improve margins in the long run. The restructurings are naturally dependent on shareholders' votes and regulatory approvals and are expected to continue until the end of 2024, more than a year and a half from now. So, it doesn't appear that the company is in a revenue growth mode and is figuring out its ownership structure for now. That's a short to mid-term risk. Aside from restructuring risks, there are some good news and progress toward improving the company's financial strengths.

Besides that, Canopy Growth is still in a lot of financial trouble, including negative free cash flow, and it may still need to raise more capital or borrow to keep building the business. The bottom line is that this company has growth potential and the right strategy but is struggling with many financial troubles. Things are moving in the right direction, but full recovery takes time and capital. Should I Add To Canopy Growth Stocks?If I park aside the fact that I bet on it back in 2018, I won't invest in CGC now. I wouldn't add to my holdings, even though we can now invest at 0.7 times book value and 2X sales. The price to book value lower than one reflects all the restructuring to convert notes and debt holders to common shareholders. That's not good for the current shareholders. And at $1.5 per share, investors are already baking twice the revenue growth in the price. I don't believe CGC is an undervalued stock, even at the current levels. Does this mean CGC would die and go away? That's unlikely. It still holds more than $500M in cash, and any legalization news in the U.S. will bring momentum to the stock. So what should I do with my 65 shares if I don't believe it is an investable stock?

Which Cannabis ETF Is A Good BuyFor example, an ETF focusing on the cannabis industry with low or reasonable management fees and large enough assets under management can be a good choice.

Most investors are familiar with Alternative Harvest ETF, ticker MJ. It's not a bad choice, with $230M in assets under management, 37 holdings, and more than seven years of operations history. But, with a 0.75% management fee, it is an expensive ETF. Alternatively, Global X Cannabis ETF, ticker POTX or Cambria Cannabis ETF (Ticker TOKE) can be good choices, too. I prefer Cambria Cannabis ETF because of its low 0.45% management fee and exposure to pharmaceutical companies active in the cannabis research space among its top 25 holdings. It is run by Cambria ETF Trust, a company by Meb Faber, a very logical, steady, and value-driven investor. I trust his judgment. The risk with Cambria Cannabis ETF is that it has a very low asset under management around $11M, which adds the risk of running out of money and liquidation if the prices do not recover soon. I choose to sell my CGC shares, use the loss for tax loss harvesting, and then buy a few shares of Cambria Cannabis ETF to bet on the cannabis market's growth rate in the coming years. Reminding you that this isn't investment advice. Now it's your turn to do your research. I leave a link to MJ's ETF Card and CGC's stock card on our platform so you can research them too. Also, don't forget that you can get a full list of all stocks in the cannabis industry by typing cannabis in the show notes. I leave a link to that list in the show notes too. If you have a better strategy to bet on the cannabis industry, share it in the comments so we can all learn from each other. I'll see you next time. Watch this episode on YouTube KEY POINTS

OVERALL MARKET

The Federal Reserve is considering tapering back its economic support soon, and the market dropped in response.

The market indices ended the day in the red once again.

We discussed the remarks by some Fed officials about the tapering of some favorable monetary policies. We received more concrete evidence for it today. The market's slide today is mostly due to the Federal Reserve’s July meeting transcripts that were released today. It shows that some members of the Fed were looking to reduce its asset-buying practice sooner rather than later, possibly as soon as this year. These members used the price stability and employment numbers as examples for why the government could ease off on supporting the economy. In response, stocks took a noticeable dive today. GET THE DAILY MARKET RECAP

Did you know you can get your Daily Market recap report on YouTube, listen to it on our Podcast, or get it in your inbox?

Watch it, Listen to it, Or, read it. Sign up for a free Stock Card account to get the report in your mailbox every day. WHAT'S UP?

Both Lowe’s (LOW) and Home Depot (HD) posted earnings this week, but share prices have gone opposite directions.

Today, I was browsing the list of winners on Stock Card and Lowe’s Companies (LOW) caught my eye. Lowe’s is the second-largest home improvement retailer in the world, so I wondered what could have moved the stock 10% in a session. Before today, the stock was at its lowest point in nine months. It seems that it was sliding quickly based on Home Depot’s (HD) subpar earnings report from two days ago. Investors looked at the HD's disappointing same-store sales growth and assumed Lowe’s would share the same picture.

Fortunately, Lowe’s had decent earnings and a good financial outlook today, which was enough to please the pessimistic investors. Home Depot’s CEO had blamed inflation such as lumber prices for its impacted sales, and while that certainly affected Lowe’s as well, its management is taking a more optimistic approach. Home Depot didn’t give a financial outlook due to rising COVID cases, yet Lowe’s raised its forecast for the rest of the year despite acknowledging that there was uncertainty. Lowe’s Stock Card is a nice 3-greener. Home Depot has similar ratings, but its stock price is a little more expensive, and it has posted a worse return on investment over the past year, or three, compared to Lowe’s. If you are trying to pick between these two home improvement giants, Lowe’s is looking like your better bet. I don't own either of the two. ETF SPOTLIGHT

A new development in gene-editing technology gave investors the conviction to double down on gene-editing stocks.

As part of my market research today, I noticed the number of gene-editing stocks that ARK Invest picked up yesterday on its trades tracker on the ARK website. It got me curious as to why Cathie Wood and her team decided to scoop up so many genome shares this particular week.

Some of you who follow my portfolios on Stock Card know that I’m a big fan of the future of gene editing. It’s a megatrend that will be shaping much of our future! A while back, I split $10,000 between 10 gene-editing stocks and I’m planning to hold them and go long. Back to ARK, according to ARK Invest's latest newsletter, there’s been a great breakthrough from the researchers at Harvard and Howard Hughes. They call the new technology “prime editing,” and it’s going to help us treat a wider range of conditions, and do it more effectively. The main advantage to prime editing is how much neater the process is when editing a strand of DNA. Prime editing allows researchers to “copy” new information onto DNA without risking damage. This is another step towards gene-editing that can benefit our entire society. That perfectly explains why Cathie and her team got a stronger conviction about the future of gene editing stocks. While I picked 10 gene-editing stocks to ride the wave, it's also possible to buy gene-editing-focused ETFs and simplify your process. Here’s two I like:

Let me know in the comments if you’re joining me as a shareholder of the megatrend that is gene-editing! FEATURED PARTNER PORTFOLIO

Stock Card partner Brian Feroldi breaks down Shopify (SHOP) in his newest video.

Folks, you know that here at Stock Card, we like to partner with successful investors who can share their research, stock picks, and analysis with you. Brian Feroldi & Brian Stoffel run a YouTube channel where they break down and analyze stocks we all want to own.

Yesterday, they released a video where they dug into Shopify (SHOP) stock. I would highly recommend that you check out their video! Also, both Brians are intelligent investors who share their portfolios on Stock Card on the Stock Picks page. Brian Feroldi runs two: a Quality Checklist Portfolio and an interesting Anti-Portfolio, which consists of the stocks he reviews but doesn’t think quite stack up. Brian Stoffel also has two portfolios: Fragile Portfolio and Anti-fragile Portfolio. Make sure to follow them both on Stock Card to be notified when they add a stock to their portfolios. WANT TO RECEIVE THIS DAILY STOCK MARKET REPORT IN YOUR MAILBOX? |

Categories

All

Archives

March 2024

|

RSS Feed

RSS Feed