Master your fundamental research. Join 79,627 investors who trust our platform and content.

Save 54+ hours of fundamental research with free access to Stock Card.

We only ask your name and email address.

KEY POINTS

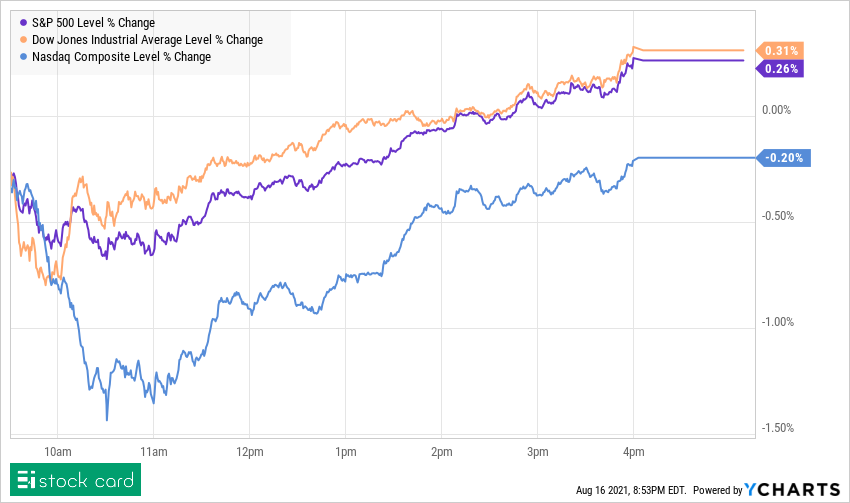

OVERALL MARKET

The market began the week with mixed numbers, as some Fed officials called for a tapering of bond buybacks.

The market indices ended the day mixed.

The S&P 500 and DOW Jones hit new records by the close today, while the NASDAQ slipped slightly into the red. There hasn’t been much happening today that moved the market, and it shows in the indices. One piece of noteworthy news was on The Wall Street Journal about some Federal Reserve officials beginning to call for a tapering of bond buy-backs next month at the Fed's upcoming meeting. Bond purchases are meant to support the economy by encouraging lending and spending, and tapering those buy-backs is part of returning to a more normal economy. However, opinions remain split on whether this step should be taken so soon or not. We still have to wait for the Fed's meeting to hear about their official stand on the matter. Let's keep an eye on them. GET THE DAILY RECAP

Did you know you can get your Daily Market recap report on YouTube, listen to it on our Podcast, or get it in your inbox?

Watch it, Listen to it, Or, read it. Sign up for a free Stock Card account to get the report in your mailbox every day. ETF SPOTLIGHT

The Electric Vehicle megatrend is shaping the future, and two EV ETFs may be a way to invest in it - IDRV and BATT.

Electric Vehicles, or “EVs,” are one of the megatrends shaping society. It's no accident that EV stocks created so much buzz in the market last year. For one, the EV battery and vehicle costs are declining rapidly, encouraging automakers to pledge to fully or partially transition to EV. Also in favor of electric transportation is climate change-friendly policies by governments around the world. These are creating the infrastructure required to make the transition from combustion engines to EVs. For example, the Biden administration's infrastructure bill focuses on developing EV charger networks across the U.S.

That's why the EV megatrend is one of the trends every investor should consider in his or her portfolio, especially if you are investing for the next decade or so. But, it's very difficult to decide which EV stock is going to win the market. Is it pure-play car makers like Tesla (TSLA) or old-timer companies such as Volkswagen (VW)? When it comes to megatrends that are in early innings, and it's hard to figure out which company would be the winner, one strategy is to invest in a well-managed ETF. Ideally, one that is putting a diversified basket of such stocks together and charges a reasonable fee. I took a look at a few EV-oriented ETFs today. Here are two of them I found worth your attention: The iShares Self-Driving EV and Tech ETF (IDRV) is a fund that tracks notable transportation companies that develop autopilot systems, and of course, electric vehicles. I came across this ETF on Nio’s (NIO) Stock Card. NIO is one of the top 25 holdings of this fund. Under the Valuation section, we can see that this fund is considered cheap to buy right now and has a great forecast for growth in the future. Scrolling down even further, it looks like the ETF gives you a wide range of exposures regarding countries, sectors, and market cap. This can be better than investing in something like the S&P 500. Another prominent ETF is the Amplify Lithium & Battery Tech ETF (BATT). This particular fund is focused on lithium battery technology that powers the EV industry. In the same sense that gas mileage is a major selling point for vehicles, the same goes for electric car batteries. Investing in the future of lithium batteries gives you plenty of exposure to the EV boom, and this ETF is a great opportunity for that. Once again, you can see that BATT is reasonably priced but has reasonable risk as well. Make sure to pay attention to the details here! If you expand the risk section, you’ll see that the “turnover” rate for stocks here is 131%, meaning that the fund managers are doing more trading than holding. Just something to be aware of before you park any money there! If you have a favorite EV ETF, let me know in the comments. I'm still looking to find the best one to invest in and benefit from this megatrend. WHAT'S DOWN?

EV leaders' stock price drop shows how Tesla and NIO plan to compete with global automakers that are entering the EV sector rapidly.

Speaking of the lithium battery ETF, one of its top 25 holdings happens to be Nio Inc. (NIO). Nio is one of the most prominent EV companies in China. Today, Nio shares were down nearly 6% after one of its SUVs was reported to have crashed while driving on autopilot, killing the driver. On Nio’s Stock Card, you’ll see that it has great sales growth and a strong balance sheet. Despite this, setbacks like today are inevitable as the driving systems are refined. It’s hard for investors and regulators to brush off serious issues like these. Today was not the hottest day for the stock, nor other EV companies, which may mean a chance to pick up shares if you can tolerate volatility like today.

Tesla (TSLA) also fell in tandem with Nio today, dropping more than 4%. This is due to a similar situation in the U.S. The National Highway Transportation Safety Administration, or NHTSA, filing an investigation into Tesla’s autopilot feature. The filing cites at least 17 injuries and a death concerning the Autopilot system developed by the company. The NHTSA also referred to 11 instances where a Tesla driving on Autopilot hit emergency responders or their vehicles. An exciting takeaway on both NIO and TSLA is that the EV megatrend and the autonomous or autopilot developments are merging, as leading EV makers try to differentiate themselves from old-time car makers who are entering the EV market in droves. You can find Tesla as a top 25 holding of the iShares Self-Driving EV and Tech ETF (IDRV) that I mentioned earlier. The case to invest in NIO and Tesla is shifting from EV makers to autonomous car makers, which is a noteworthy change if you are holding these stocks. It's good that they are making a move, but it also means many more years of volatility as these companies sort through the challenges related to autopilot technology. WANT TO RECEIVE THIS DAILY STOCK MARKET RECAP IN YOUR MAILBOX?KEY POINTS

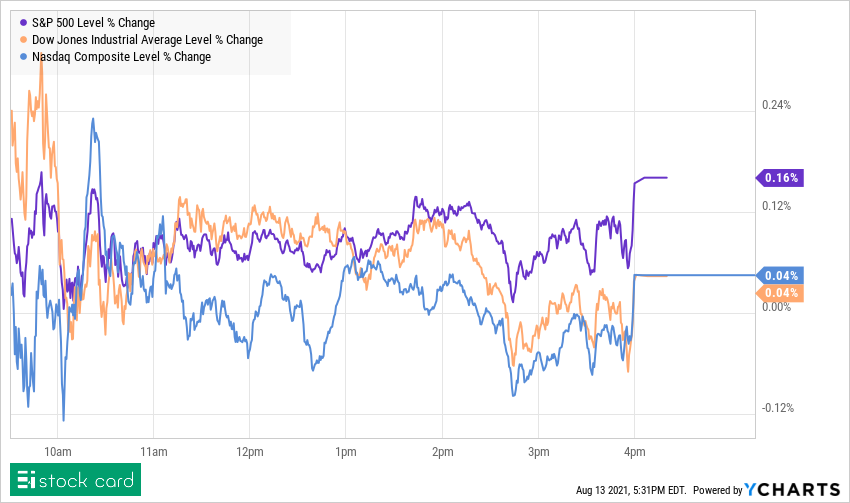

OVERALL MARKET

Despite a loss of confidence from consumers, the stock market continued to climb by the end of the trading week.

The market indices ended the day in the green.

Contradictory forces are shaping the market's sentiment. Thursday’s jobless claims report from the Bureau of Labor Statistics painted a better economic picture, with a lower number of new claims for the third row in a week. However, a Survey of Customers by the University of Michigan showed consumers' surprising loss of confidence at the beginning of August. This could be due to the growing concerns around the COVID Delta variant. In the end, positive sentiment won over, and all three indices finished the week in the green. GET THE DAILY MARKET RECAP

Did you know you can get your Daily Market recap report on YouTube, listen to it on our Podcast, or get it in your inbox?

Watch it, Listen to it, Or, read it. Sign up for a free Stock Card account to get the report in your mailbox every day. WHAT'S UP?

Yum Brands (YUM) is “defying” drive-thru norms with its new experimental Taco Bell location.

Folks, recently, we have been exploring some food companies that are innovating how we eat. For example, we discussed Wendy’s (WEN) ghost kitchens. From plant-based foods to fermented ingredients and new ways to prepare and deliver food, the way we eat is changing rapidly, and that's why the team at Stock Card manages the “Future of Food” portfolio.

Today's winner stock is a company that is innovating how food is delivered to us. Yum Brands’ (YUM) Taco Bell franchise is defying the norm of fast-food drive-thrus. I mean that quite literally! Taco Bell is breaking ground this month on an experimental “Defy” drive-thru-only building. Fast food companies across the nation pivoted to depending on contactless food services, like drive-thrus, during the pandemic. Many went through quite a lot of operational challenges to deliver food efficiently in this new world, and now we see food delivery innovation popping up all around us. Drive-thrus and mobile order windows are great ways for companies to increase sales revenue, and this new step is taking the idea all the way. Yum! Brands had its earnings call 2 weeks ago, which surpassed expectations. The investor reaction brought the stock up from $122 to $130, and it has continued to climb steadily since. The company also owns KFC and Pizza Hut, among other brands. Its Stock Card shows good profitability, revenue growth this fiscal year, and free-cash-flow generating operations. With 1.5% in dividend yield, the stock could easily fit into a dividend-focused portfolio, although there are some concerns about the amount of debt it carries. If the innovations such as the new drive-thru pay off, Yum Brand can expand it across all its brands and run a much more profitable business. It is worth watching, especially if you are a dividend seeker. Yum Brands is shaping the future of food by reimagining the drive-thru. WHAT'S DOWN?

Does Tattooed Chef’s (TTCF) dip mean it’s time to buy?

Speaking of companies on the mission to shape the Future of Food and get into our Future of Food portfolio, I want to revisit an old favorite of mine. Tattooed Chef (TTCF) has been on my personal 2021 watchlist for a while. You can find this by searching “2021 watchlist” on the Stock Card portfolio page as well. I’ve been waiting around for this stock to drop so I could snatch it up at a good price. My wish came true today!

TTCF shares were down 16% by the close. It's a ready-to-eat, plant-based food startup that focuses on the frozen aisle for now and serves you things like Budda Bowls and cauliflower pizza. It was founded in 2018, but despite its young age, its growing revenue rapidly and is already profitable. Earlier today, the company released itsearnings report for this quarter. Tattooed Chef saw a 46% growth in revenue this year, which was great, but investors latched onto some future guidance. It forecasted a lower gross margin and a substantial loss in adjusted earnings before interest, taxes, depreciation, and amortization, known as EBITDA. As for last quarter, EBITDA was a loss of $5.9 million, yet future guidance from the company is expecting an even more significant loss of $14 to $17 million. It’s no wonder that the company has a short interest of 14%, as I see on its Stock Card. The reason for the loss of profitability, according to the management, is reinvesting into expansion. Investors forget that the company is just 2-3 years old and already has distribution deals with Walmart (WMT), Costco (COST), Target (TGT), Sam’s Club. Thanks to the latest price drop, I’m considering picking up some more shares on Monday to enjoy a lower price. Tattooed Chef is shaping the future of food by delivering better pre-made food in the grocery aisles. NEW STOCK CARD FEATURE

Announcing: Stock Card’s new ETF cards!

Folks, I've already told you a few times and want to share this exciting news once again that we rolled out a significant new update to Stock Card. You can now research ETFs using the same easy-to-use and intuitive visualization and color-coding on Stock Card. ETF Cards have been one of the most requested features you have asked for in the last 12 months, and your wish is our command.

A couple of days ago, I uploaded a quick rundown to show you how to research ETFs using the new ETF Cards. For a more in-depth explanation, I'd like to invite you to check out the demo video. WANT TO RECEIVE THIS DAILY STOCK MARKET RECAP IN YOUR MAILBOX?

Which internet and social media company will dominate the market next? Is it either Snap (SNAP) or Sogou (SOGO), and whether either of them a safe buy as a long term investment?

This is Sailesh Tirupasur. I'm a part of Stock Card's summer internship program in 2020, and this post is a part of my Stock Battle series. I don't own these two stocks, and my goal here is to study them to decide whether to invest or not. These stocks are apart of our Companies Shaping the Future stock list. If you want to see other stocks in this category, click here. Sogou's research: Sogou (SOGO) is a Chinese search engine with a language input technology that captures Chinese expressions and phrases on the internet. Recently, the company's shares were moving up, which has speculative investors interested in the stock. Its recent earnings report shows that the company's search business is outperforming the market despite the pandemic. Total revenue grew by 2% compared to a year ago and reached $257 million, and the company is profitable with a 12-month EPS of $0.15. However, compared to the industry benchmark, it has a smaller gross profit margin, which is concerning, and the revenue growth, while positive, is small.

Snap's research:

Snap (SNAP) calls itself a camera company. However, most people know the company by its social networking app Snapchat. Since going public in mid-2017, it has evolved its app in many ways. Starting from a simple image and video app, Snap has added image enhancing, ads, video content, games, and augmented reality capabilities. While seeing steady growth, Snap has recovered quite well from the low of March. Its recent earnings report shows that despite its struggles with profitability, sales growth is robust. However, the company's gross profit margin and 12 month EPS are both negative and lower than the industry benchmark.

Final decision:

While Sogou has a massively larger audience to tap into, Snap already has its position as a market leader and is widely popular in the U.S. among the younger crowd. Moreover, the company's focus on enhancing its platform beyond basic social media features and into augments reality capabilities are some of the features that may lead to its rapid growth in the future.

Which renewable energy company is a more lucrative investment? With Plug Power (PLUG) and Canadian Solar (CSIQ) taking different approaches to renewable energy, which company is poised for growth in the future?

This is Sailesh Tirupasur. I'm a part of Stock Card's summer internship program in 2020, and this post is a part of my Stock Battle series. I don't own these two stocks, and my goal here is to study them to decide whether to invest or not. These stocks are apart of our Companies Shaping the Future stock list. If you want to see other stocks in this category, click here.

Research and analysis:

Plug Power (PLUG) and Canadian Solar (CSIQ) are two leaders in the renewable energy industry. The two companies have a history of being at the forefront of the extremely popular niche and are pioneering developments in fuel cell and solar panel technology.

Plug Power's analysis: Plug Power is an innovator of modern hydrogen and fuel cell technology. According to the company's quarterly earnings release, "it has revolutionized the material handling industry with its full-service GenKey solution, which is designed to increase productivity, lower operating costs, and reduce carbon footprints reliably and cost-effectively." Based on Scott Levine's analysis, shares of Plug Power are up 180% year-to-date due to investors growing more confident that the company is on track to meet management's 2024 projection of generating sales of $1.2 billion and an operating income of $170 million. Plug Power has also strengthened its business profile by acquiring two companies in June that will aid in the business of hydrogen generation. While the company has a track record of growing its top line, many experts are wary of its future. The company's history of diluting shares also has investors skeptical about the future of the company.

Canadian Solar's analysis:

Canadian Solar is an integrated provider of solar power products, services, and system solutions. While many solar panel companies have gone bankrupt, Canadian Solar has thrived over the past decade, and investors are quite confident in its future. The solar panel expert set a goal of solar module shipments this year and expects to increase its growth rate by over 15% by the end of this year. Canadian Solar also has a strong focus on the energy storage market with a massive 2,820 megawatt-hours of storage projects. According to the company's Stock Card, the company's profitability seems quite positive last year, with an EPS growth trend of 10%. Its last quarter's profit margin is also at around 27%, which is over 10% higher than industry benchmarks. One prevalent risk that financial analysts like Scott Levine discuss is that solar panel businesses tend to sacrifice pricing power for market share. Final decision: Although the fuel cell market is expected to grow by around 13%, Plug Power's financials seem to be weak compared to Canadian Solar's. Canadian Solar has a long history of profitability and growth as well as the market for solar panels being expected to grow substantially.

With tech companies like Tencent Holdings (TCEHY) and Alphabet (GOOG) leading the way for everything from internet content to gaming, which of these companies is better investment? Which company has bigger growth potential, especially after the pandemic has shaken up the market?

This is Sailesh Tirupasur. I'm a part of Stock Card's summer internship program in 2020, and this post is a part of my Stock Battle series. I don't own these two stocks, and my goal here is to study them to decide whether to invest or not. These stocks are apart of our Companies Shaping the Future stock list. If you want to see other stocks in this category, click here. Stock research and anaysis: Tencent and Alphabet are two of the world's most influential tech companies. Tencent's businesses consist of market-leading gaming, mobile messaging, advertising, cloud, and media streaming businesses. Tencent's stock has surged nearly 50% over the past 12 months, and many investors are hyped about the Chinese internet giant's growth potential. Much of this surge has to do with Tencent being the largest video game publisher in the world. Tencent’s massive video game publication list includes League of Legends, Clash of Clans, Honor of Kings, and has a stake in Epic Games and Bluehole. According to Leo Sun, a tech and consumer goods specialist, the gaming section generated 35% of Tencent's revenue last quarter and grew substantially due to COVID-19 forcing people to stay at home. Tencent's online advertising business, its second most profitable sector, was also flourishing due to online education, and e-commerce companies trying to push ad purchases to stay-at-home consumers. The increase in revenue in ad purchases offset the slower growth of the ad purchases in the travel, auto, and consumer goods markets due to COVID-19 . Overall, Tencent is a stable and diversified company that has few risks. One major risk for the Chinese internet giant is that it has some major competitors. Companies such as ByteDance and Alibaba (BABA) are fierce competitors in the internet space and control a majority of the market share. Alphabet is a large tech company that owns Google and is fairly diversified in internet content and information. Alphabet's Google dominates online searches, its Android OS leads the smartphone market, and its YouTube division reached over two billion users. The company's stock has grown roughly 35% over the last 12 months, making it a bit less than Tencent. The slower growth rate could be due to the Alphabet's reliance on Google's advertisement business, which generated 82% of the company's revenue last quarter. This dependence on advertisement revenue leaves the company a bit more exposed to the market's dynamics and sensitive to the cost of acquiring traffic. In the latest quarterly earnings report, Google's traffic acquisition costs remained steady year-over-year at 22% of its total ad revenue. However, that percentage could rise as the COVID-19 crisis throttles ad purchases, and fierce competitors, such as Facebook and Amazon, expand their advertising platforms. Moreover, in the recently announced quarterly report, Alphabet's revenue rose 13% annually in the first quarter and seems to be going steady with a 3% increase today. The slower than expected advertisement revenue growth is a risk investors in Alphabet have to consider. Considering that both companies are the heavy-weight titans of their respective markets and industries, which one is a better investment choice?

Final decision:

While both stocks are solid long term investments, I'd buy Tencent for its better-diversified business, stronger financials, and stronger growth rates.

|

Categories

All

Archives

March 2024

|

RSS Feed

RSS Feed