Master your fundamental research. Join 79,627 investors who trust our platform and content.

Save 54+ hours of fundamental research with free access to Stock Card.

We only ask your name and email address.

|

Snap (SNAP) is a $13B technology company, that almost every teenager uses its app to connect with friends. It has successfully engaged and satisfied its users but not so much its investors. Its stock is down more than 50% since its IPO in 2017. Many attribute Snap's fall to TikTok's fierce competition in recent years. Is that reason justified, or is the 50% drop in the stock price a buying opportunity? I'm Hoda Mehr, founder, and CEO of Stock Card, and on this blog and its accompanying YouTube channel and Podcast show, I share detailed fundamental analyses and interesting investment stories. This post is part of a series I started last week to research companies I own that are down significantly from their all-time highs to decide whether to buy more or sell and allocate money to other companies. I've already researched Canopy Growth (CGC), and Fastly (FSLY), and I'll continue with this series for a few more weeks. Remember, these videos are for education and sharing ideas and not advice to buy or sell any securities. TikTok Is The Stock Market's BoogeymanTikTok's influence on the stock prices of companies such as Snap is like a stock market boogeyman story. In general, investors assume the rise of TikTok means the fall of Snap, Facebook, Instagram, YouTube, and other content platforms. On the surface and intuitively, this seems true. TikTok is one of the most downloaded and used content consumption platforms in the U.S. Anything that consumes people's time leaves less time for engaging and interacting with other applications such as Snap. However, in investing, relying on only your intuition can be catastrophic. We must dig into the facts and confirm or reject our intuition. Today. We will research Snap's fundamentals to bring logic to our intuition. Let's talk Snap now. TikTok Isn't Killing SnapPeople, I'm 41 years old and have never used Snapchat. But I own its shares. Why? In 2019, I researched the stock fundamentally when it was trading at around $17 per share and concluded it's a financially solid company worth owning. Here's the link to that 2019 fundamental analysis in the show notes if you want to go back and watch or listen to it. But in summary, revenue was growing 48% year over year. The average revenue per user was about $2, significantly lower than Facebook's average, highlighting a significant revenue growth opportunity for Snap. Its daily active users were around 13 million, and there was no TikTok to worry about. Fast forward to 2023, and the stock is down to roughly $8 per share, 50% lower than when I researched it in 2019. It still makes money primarily from advertising. However, it added other revenue sources such as subscription revenue from more than 3 million subscribers and enterprise SaaS revenue from selling its AR-based Shopping Suite functionality enabling customers to try retailers' products using AR before buying. It made $4.6B in revenue in 2022, up 35% per year compared to 2020. The company's daily active user is now up to 383 million, from the 13 million I told you about in 2019. In the United States, users open the app more than 40 times daily. So compared to 2019, the company is in a much better position, but the stock price is down 50%. In comparison, TikTok is expected to make $10 Billion in ad revenue in 2023, with its daily active users across iOS and Android devices being around 45 million, excluding the Chinese version of TikTok. Snap is competing head-to-head with TikTok's short-form video platform. Its new feature, Spotlights, is a TikTok-comparable short-video sharing feature with more than 5 billion Snaps created daily. The company continues to focus on investing in Augmented Reality (AR), with 250 million users interacting with AR features. The interesting and unique aspect of Snapchat is its myopic focus on the younger generation of 13- to-34-year-olds. The platform focuses on becoming the first app kids download when they get their first mobile phone. With its focus, it has managed to attract 75% of its target market in 20 countries representing more than 50% of the global advertising market. In comparison, TikTok covers a much broader demographic. For example, roughly 3.5% of TikTok's audience is above 50 years old. In summary, Snap has more engaged users daily and has been able to grow its user base just like TikTok. But Snap makes half the revenue TikTok does. If TikTok was Snap's problem, we should have seen user and engagement losses for Snap. That's not the case, meaning Snap's stock price decline is not because of direct TikTok competition. So if TikTok isn't a problem, what is? Snap's Quarterly Earnings Report Recap

Those are some serious concerns about the company and have nothing to do with TikTok or the global advertising market. Snap's Fundamental AnalysisLet's turn the conversation around and explore whether Snap has a way to redeem itself. Firstly, can it resume revenue growth? Aside from external factors, such as the advertising market's short- to mid-term recovery, Snap has to convince advertisers to spend their dollars on its platform. Typically, revenue is a lagging indicator. That means revenue growth is the last financial metric showing a company's financial strength. Things like the number of users and growth in active users are early indicators. Snap's user and engagement growth could signal higher revenue a few quarters down the road. Snap's investment in AI and machine learning isn't only focused on user engagement and is dedicated to enhancing advertisers' ability to get and measure the return on their advertising dollars spent on Snap. The investment would pay off, I believe. I based that belief on seeing how the management has grown users and engagement and cut costs enough for the company to generate free cash flow in the last two quarters. Those tell me the management is capable of delivering on their plans. Moreover, despite more than $1B in stock buybacks and high R&D expenses, Snap still has more than $4B in cash and marketable securities, and it doesn't fear immediate balance sheet concerns. So let's summarize what we've learned about Snap:

Is Snap A Buy Now?If the best investment strategy is to invest in a company with a lot of upside potential and not much downside risk, let's do some quick math to decide whether Snap fits that strategy. To set the foundation, let's make some valuation comparisons. Snap is priced at 3.5 times its sales. META is priced five times its sales. TikTok isn't a publicly-traded company, but we can do some math. According to Bloomberg, TikTok U.S. can be a $40 to $50 Billion dollar company. With an estimated $10B in revenue in the U.S., the company is priced at 4 to 5 times its 2023 revenue. With those price-to-sales comparisons, Snap is an undervalued stock. What's the optimistic scenario? Optimistically, if we believe in the assumption that higher user engagement will eventually translate to revenue growth, the upside is that the company will grow its revenue by 15% starting next year and gets a price-to-sales ratio of 5 which is the current META or TikTok's price-to-sales ratio. In five years, Snap would be a $40B company or 2.5 times bigger than today. What's the pessimistic scenario? Snap can fail on all its revenue growth targets, use up all its cash, and become a worthless company. What's a bit more realistic scenario? Snap's revenue stays flat for another year or two and slowly recovers to its historical 15% year-over-year growth in the next five years. Its R&D expenses and stock-based compensations stay elevated, preventing higher valuation multiples than today. With those assumptions, the company has about 20% growth potential in the next five years. Knowing all that, what do we do with Snap shares: There is at least 20% upside potential in Snap's shares. If we are patient and keep looking, we will find better investment opportunities to grow our investment faster than Snap. However, considering that upside, I don't see any reason to scare away and sell my SNAP shares now because the company isn't in immediate danger. For me, Snap goes in the hold-until-better-opportunities bucket. However, I would have looked for better investment opportunities if I didn't own Snap shares. 20% realistic return in five years isn't a good investment, especially in an environment where the risk-free investment return in CDs is already at 5% per year. It's your turn to share your research. What other investment opportunities justify selling Snap at a loss and buying up those shares now? You can go to Stock Card and look up Snap's Stock Card to start your research. Click here to jump to it's Stock Card. Next week, I will be back with another beaten-down stock fundamental analysis, for now, go ahead and watch the rest of this series by clicking on the link in the show notes. I'll see you next time. Fastly, ticker FSLY, was one of the hot stocks during the COVID-19 pandemic. The company went public in 2019 and started its first trading day at around $21 per share. By October 2020, its stock was trading at nearly $130 per share, up by more than 400% in roughly a year and half after its IPO. Two years after, by the end of 2022, the stock lost almost all of its value, trading at $7 per share. The rise and fall of Fastly is a classic example of a pandemic stock. Is the post-pandemic price slump an opportunity to buy shares? Let's talk about that! I'm Hoda Mehr, founder, and CEO of Stock Card, and on this blog and its accompanying YouTube channel and Podcast show, I share detailed fundamental analyses and interesting investment stories. This post is part of a series I started last week to research companies I own that are down significantly from their all-time highs to decide whether to buy more or sell and allocate money to other companies. Last week I researched Canopy Growth (CGC), the link in the show notes, and I'll continue with this series for a few more weeks. Remember, these videos are for education and sharing ideas and not advice to buy or sell any securities. The Two Categories of Pandemic StocksThe COVID-19 pandemic created several interesting examples of rapidly growing stocks to unbelievable all-time highs and subsequent crashes to unimaginable all-time lows. Fastly is one of those stocks. We all know that the pandemic drastically increased the demand for content online. Accordingly to Fastly's blog, during the pandemic, some countries, such as Italy, experienced more than a 100% increase in online traffic resulting in a drastic decline in internet speed. Fastly was there to speed up the internet's speed. As the pandemic subsided and the demand for online content went back to its normal rate, Fastly's stock price followed suit. This part of the story is quite common across the so-called pandemic stocks. However, they are split into two categories:

Fastly (FSLY) Fundamental AnalysisAs always, we start any company's fundamental analysis by understanding what the company does. In lament terms, Fastly makes the internet faster. When you buy a ticket from Ticketmaster for the next event you plan to attend or are loading an article on the New York Times website, Fastly is working behind the scenes to load that page for you oh so Fastly. Fastly's technology is called CDN or Content Delivery Network. Its market is expected to grow by 18.31% per year between 2022 and 2032. If you want to see Fastly's competitors in the CDN market, type content delivery network or CDN in the search bar on StockCard.io and get the full list of CDN companies, or click here to get the list. Back to Fastly, the company is growing its revenue by double digits. Its gross margin is hovering close to 50%. It has a solid balance sheet with over $600M in cash and cash equivalent and an acceptable 0.7 times debt-to-equity ratio. If things are acceptable and reasonable, why is the stock price down significantly since its 2019 initial public offering?

Is Fastly (FSLY) A Buy Now?Knowing all the above analysis, what do we do with Fastly? Buy the post-pandemic dip, or stay away? An optimal long-term investment thesis for any company is strong fundamentals with low market expectations. The more I grow into my career as an investor, the more inclined I'm to find investment opportunities that meet those two criteria. Fastly, unfortunately, doesn't meet either of those criteria. It's growing at the same pace as the market, in the 20% range. And Investors are already pricing the stock five times its sales, and the path to profitability is still unclear. Those tell me the company isn't yet fundamentally solid, and the market's expectation is already baking in a five-time growth in revenue. Fastly's Rule 200 AnalysisThere is one more analysis I'd like to run on Fastly. It's known as Rule 200. It's a quick formula the venture capitalists use to measure a growth company's financial strength, and I'd like to use it to measure the strength of tech stocks I invest in. For Rule 200 to give a company a thumbs up, the sum of its revenue growth, gross margin, operating margin, and net revenue retention has to be higher than 200. Fastly's revenue grew 22.12% last year. Its gross margin is 48.48%.The operating margin is - 56.90%, and its net revenue retention is 119%. Sum that all up, and we get 132, significantly lower than 200. The negative operating margin would have been fine if Fastly had been able to grow much faster or had a significantly higher gross margin. But as it stands today, the company doesn't meet the Rule 200 criteria either. No wonder high-growth technology investors such as Cathie Wood sold all her fund’s investment in Fastly in mid-2021. Analysts' Target For Fastly (FSLY)It's important to note that earlier in the year, in mid-Feb, several analysts, including Bank of America analysts covering Fastly) upgraded their Fastly recommendations from sell or hold to Buy with price targets around $16 to $26 per share, sighting gross margin improvement and cost reductions. In April 2023, as I'm doing this research, we are already there at roughly that target price. So sadly, if you invested in the company at its IPO or when it was priced at $50 or $100 and held on to them like me, we may have to wait a long time to recover to those levels, if ever.  Bottom-line on Fastly's StockYou can wait until June's investor day by the company. That's when the management is supposed to share more concrete plans for reaching profitability. However, fundamentally, unless we see another significant surge in internet content delivery needs like what we experienced during the pandemic, there is no reason to expect Fastly to return to the previous all-time highs of the pandemic era anytime soon. Now, it's your turn to share your thoughts on Fastly. Do you see fundamental reasons to buy now or hold the stock longer? You can go to Stock Card and look up Fastly's Stock Card to start your research. Click here to jump to it's Stock Card. Next week, I’ll be back with a fundamental analysis of Snap (ticker SNAP) as a part of my beaten-down research series. I'll see you next time. Put Your Money To WorkThe year was 2018-19, and Cannabis stocks were hot! All the cool kids were trading them. One of the market leaders, Canopy Growth was trading at $50 per share, and another, Tilray, was priced at more than $140 per share. Fast forward to 2023, and cannabis stocks have lost almost all their value. Both those market leader stocks are now down 98% from their all-time highs of 2018-19. Cannabis stocks are either destined for bankruptcy, and 100% value loss or they are deeply-discounted opportunities we should pay attention to now. Let's talk about that! I'm Hoda Mehr, founder and CEO of Stock Card, and on this blog and the accompanying YouTube channel and Podcast show, I share detailed fundamental analyses and interesting investment stories. The rise and fall of cannabis stocks is a classic story of investors running wild after the next big thing, pushing the prices to levels completely disconnected from the economic reality behind the companies and stocks in that sector. Then suddenly and violently, everything comes down crashing. Almost all similar stock market stories start with a new shiny sector and end with investors losing almost all their capital. I own a few shares of Canopy Growth in my portfolio, shining red hot at the bottom of the biggest losers. I purchased those shares in 2018 with a few justifications:

As Uncle Buffett puts it, if the price of hamburgers goes down, you don't stop eating them. You may even eat more. By the way, talking about my personal portfolio it's called Roll with Our CEO. This portfolio is our family's real-money stock market investments, beating the S&P 500 going back to 2014, and it's available to our VIP users to see and follow. If you'd like to access it, go to StockCard.io, create an account for free, and then use promo code "welcome" to receive 20% off of the Full VIP plan to see my entire portfolio. Click Here to Upgrade Of course, my portfolio isn't investment advice, neither are any of 100s of other real-money and idea portfolios on our platform. Use them as a resource for new ideas or validate your own ideas while doing your research. Now, how can Canopy Growth recover, grow and even thrive in the next ten years:

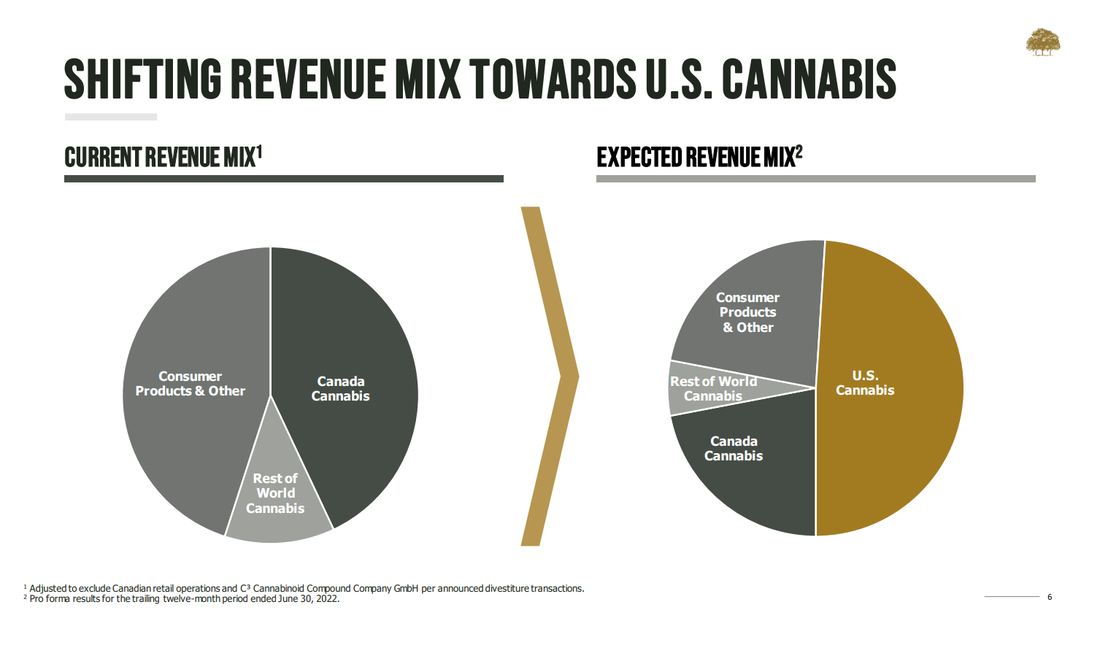

Cannabis Industry Market SizeDespite everything happening with Cannabis stocks, the global cannabis market is expected to grow by 24% between 2022 and 2026. The industry was hit by COVID-related restrictions, especially as farming and processing cannabis needs in-person human labor. But, with the pandemic restrictions almost entirely eliminated, the industry is back on a growth track. It's quite apparent that legalizing medical and recreational cannabis use is an important factor in driving growth. In the U.S. alone, 40 states and the District of Columbia have legalized medical use, and 21 states allow recreational use. Even in a state like Texas, bills are advancing to legalize medical use. While Federal level legalization is unlikely this year, President Biden has asked the Secretary of Health and the Attorney General to review cannabis's classification as a Schedule II drug which is good progress toward ultimate legalization. It also opens the door for more pharmaceuticals to start researching it as an ingredient which can lead to a significant demand increase by pharmaceuticals down the road. So, despite the stock price crashes, the cannabis industry is growing steadily. Canopy Growth (CGC) Fundamental AnalysisIf Canopy Growth can grow its revenue by at least 50% of the overall market rate, the stock will have major growth potential. Especially if you compare that with its 2022 5% revenue drop. The question is whether Canopy Growth and its management believe that can achieve such growth. Let's see what they had to say in their latest investor presentation. The company aspires to generate 50% of its revenue from the U.S. market instead of its current concentration in Canada. It's been investing in a portfolio of consumer-facing brands such as Acreage, Wana, Jetty, and TerrAscend, and plans to grow its own brands in the U.S. As a matter of fact, the company calls the U.S. legalization a once-in-a-generation opportunity.  That's a good strategy. However, the company outlined several restructuring requirements to simplify its organization, especially related to Constellation Brands' investment in the company and acquisition deals related to Acerage, Jetty, and Wanna. It's also moving away from retail operations by divesting from its Canadian retail business to cut costs and improve margins in the long run. The restructurings are naturally dependent on shareholders' votes and regulatory approvals and are expected to continue until the end of 2024, more than a year and a half from now. So, it doesn't appear that the company is in a revenue growth mode and is figuring out its ownership structure for now. That's a short to mid-term risk. Aside from restructuring risks, there are some good news and progress toward improving the company's financial strengths.

Besides that, Canopy Growth is still in a lot of financial trouble, including negative free cash flow, and it may still need to raise more capital or borrow to keep building the business. The bottom line is that this company has growth potential and the right strategy but is struggling with many financial troubles. Things are moving in the right direction, but full recovery takes time and capital. Should I Add To Canopy Growth Stocks?If I park aside the fact that I bet on it back in 2018, I won't invest in CGC now. I wouldn't add to my holdings, even though we can now invest at 0.7 times book value and 2X sales. The price to book value lower than one reflects all the restructuring to convert notes and debt holders to common shareholders. That's not good for the current shareholders. And at $1.5 per share, investors are already baking twice the revenue growth in the price. I don't believe CGC is an undervalued stock, even at the current levels. Does this mean CGC would die and go away? That's unlikely. It still holds more than $500M in cash, and any legalization news in the U.S. will bring momentum to the stock. So what should I do with my 65 shares if I don't believe it is an investable stock?

Which Cannabis ETF Is A Good BuyFor example, an ETF focusing on the cannabis industry with low or reasonable management fees and large enough assets under management can be a good choice.

Most investors are familiar with Alternative Harvest ETF, ticker MJ. It's not a bad choice, with $230M in assets under management, 37 holdings, and more than seven years of operations history. But, with a 0.75% management fee, it is an expensive ETF. Alternatively, Global X Cannabis ETF, ticker POTX or Cambria Cannabis ETF (Ticker TOKE) can be good choices, too. I prefer Cambria Cannabis ETF because of its low 0.45% management fee and exposure to pharmaceutical companies active in the cannabis research space among its top 25 holdings. It is run by Cambria ETF Trust, a company by Meb Faber, a very logical, steady, and value-driven investor. I trust his judgment. The risk with Cambria Cannabis ETF is that it has a very low asset under management around $11M, which adds the risk of running out of money and liquidation if the prices do not recover soon. I choose to sell my CGC shares, use the loss for tax loss harvesting, and then buy a few shares of Cambria Cannabis ETF to bet on the cannabis market's growth rate in the coming years. Reminding you that this isn't investment advice. Now it's your turn to do your research. I leave a link to MJ's ETF Card and CGC's stock card on our platform so you can research them too. Also, don't forget that you can get a full list of all stocks in the cannabis industry by typing cannabis in the show notes. I leave a link to that list in the show notes too. If you have a better strategy to bet on the cannabis industry, share it in the comments so we can all learn from each other. I'll see you next time. Watch this episode on YouTube |

Categories

All

Archives

March 2024

|

RSS Feed

RSS Feed